What Monthly Salary Is Needed To Afford A Home Loan?

It is always very important to work out how much you can afford to borrow from a financial institution - before you start looking for a suitable property to buy. The simplest way to do that is to either contact a bond broker (originator) for a free quote or use a bond affordability calculator to understand what you can afford when buying a home. Financial institutions such as banks uses an affordability assessment which takes into account your income and expenses to calculate whether you will be able to repay your mortgage.

Your monthly salary after tax, total monthly expenses, interest rate and loan term (years over which you will pay off your bond) are used to estimate the total loan amount you can afford with the monthly repayment amount. If you and your spouse or partner are buying a property together, then the gross "household income" can be used to determine for which home loan amount you can qualify.

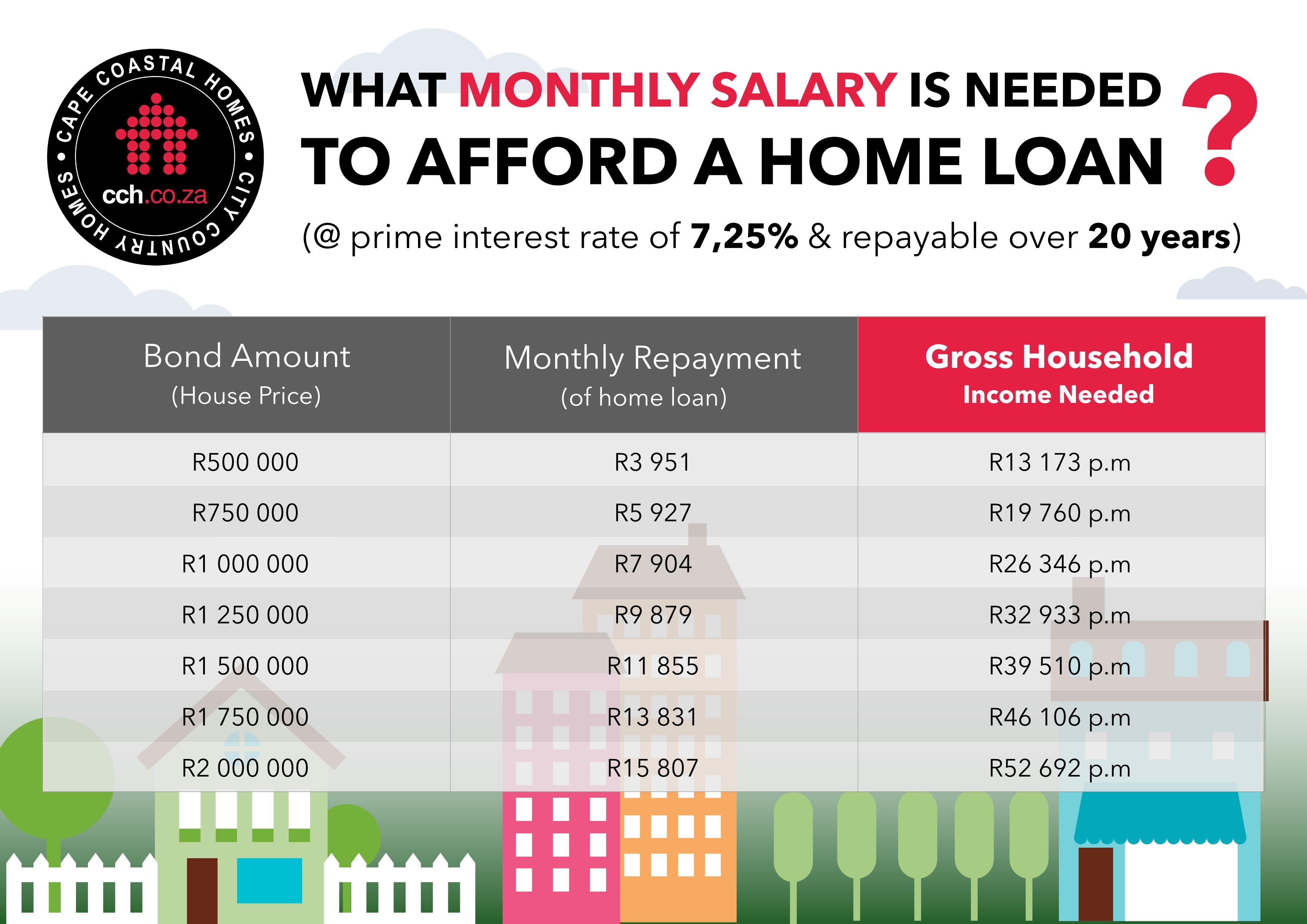

The table above showcases the most popular price ranges in the South African property market - which is between R500 000 and R2 million. In fact - about 80% of all property registrations in South Africa (during 2019) falls in the price brackets below R1,5 million.

The table shows e.g. that the gross monthly household income needed to be to buy an average entry level home (80-140 sq.m) for around R 937 000 would be roughly about R25 000 p.m., whilst the gross monthly income to buy an average medium-size house currently costing around R 1 255 000, would be about R33 000 p.m.

- Using the affordability calculator

As a general rule, you should look at spending no more than a third of your monthly income (after tax and deductions) towards your monthly bond repayments.

Calculate what you can afford using the CCH Affordability Calculator on our website

- Using the bond calculator

A bond calculator is used to calculate the monthly home loan instalments and the interest added over the loan period. This will determine your affordability level by calculating your income against main bond variables and other monthly expenses.

Calculate your monthly mortgage repayments by using the CCH Bond Calculator on our website.

When using the bond affordability calculator you also need to establish what your gross monthly income and total expenses is. The CCH calculator does provide a fairly comprehensive list of income items for both you and your co-applicant (surety) - including items such as gross salary, commissions, housing subsidy, investments, rental income and other items.

- How do you calculate your monthly income?

The most logical income item is your monthly salary - but not all salaries "are weighted the same". Some people receive a fixed amount monthly, while other people receive commissions as part of their job. It may also include other forms of income, like allowances, overtime and bonuses.

When the financial institutions estimate what income will or can be used on your affordability assessment, they need to know how likely you are to get this. Bonuses are paid mostly once a year, so they will not be able to use it as an item for your monthly income. The banks focuses on the fixed-income part which will not deviate too much and 100% of this value will be used by them as income.

The variable incomes (like commission and overtime) are not the same each month and the banks either use a lower portion of this amount or use at least a three-month average of this income.

While everyone wants to show or proof that they earn enough money to qualify for their home loan of choice, the Covid-19 pandemic has shown that it is realistic that buyers can fall short of some monthly income items at any given time. Such more uncertain income items is e.g. working overtime every month.

- How do you calculate your monthly expenses?

Most people underestimate their true expenses as they rarely do a proper monthly budget. Expenses can be divided into three broad categories:

1 Credit expenses are your monthly instalments paid from debt obligations you already have - like your car instalments or monthly credit card repayments.

2 Living expenses can be categorised as essential expenses. This includes transport, food, education, medical, water, electricity and maintenance.

3 Other expenses are for things like prepaid airtime, insurance premiums and satellite TV. These are not necessary expenses and can be scaled down.

Banks determine with each home loan application the client's your risk profile to calculate the appropriate interest rate they are willing to charge the home loan applicant. Based on this rate, the banks then calculate the home loan applicant's monthly repayment over the term of the loan.